—Michael Lyles, B1Daily

For many millennials, the frustration isn’t abstract — it’s economic. Born roughly between 1981 and 1996, this generation entered adulthood during or just after the Great Recession and has since navigated stagnant wages, rising housing costs, ballooning student debt, and inflation shocks. Compared to Generation X at similar life stages, the data helps explain why so many millennials feel priced out.

Housing: The Largest Barrier

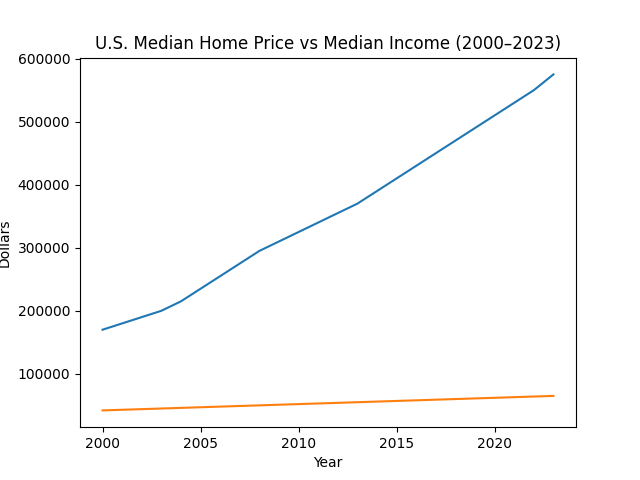

Homeownership has traditionally been the primary wealth-building vehicle for American families. Yet millennials have faced historically unfavorable housing conditions.

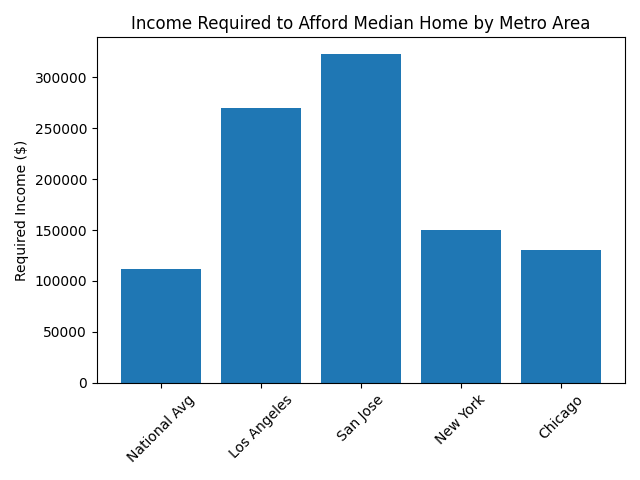

In the early 1990s, when Generation X was entering the housing market, the median home price was roughly 3–4 times median household income. In the 2020s, that ratio has frequently climbed above 5–6 times income nationally — and significantly higher in major metro areas.

Mortgage rates compound the issue. Millennials who delayed buying during the post-2008 recovery due to tight credit conditions later faced rapid price appreciation during the pandemic housing surge, followed by sharp interest rate hikes. The result: higher monthly payments even for comparable properties.

Homeownership rates among millennials at age 35 remain below where Generation X stood at the same age.

Wage Growth vs. Cost Growth

While nominal wages have risen over the past decade, real wage growth — adjusted for inflation — has been uneven. Key cost categories have dramatically outpaced wage gains:

- College tuition has increased multiple times faster than inflation since the 1990s.

- Healthcare premiums and out-of-pocket costs have risen steadily.

- Childcare expenses in many states rival or exceed in-state college tuition.

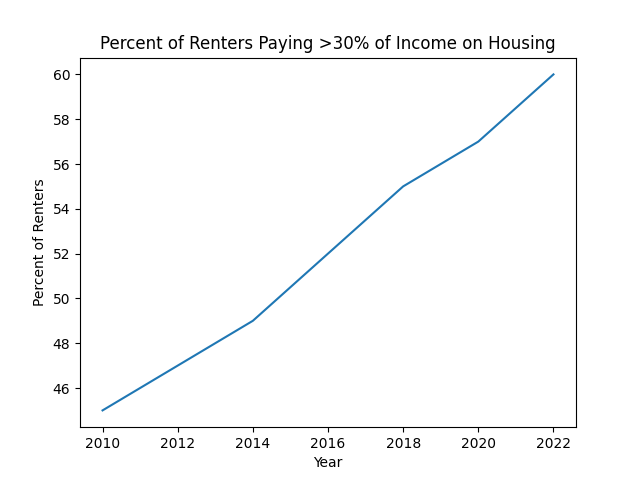

- Rent growth in major urban centers has consistently outpaced median income growth.

Millennials also entered the workforce during the weakest labor market in decades. Graduating into the 2008–2012 recession years had lasting “scarring effects,” reducing lifetime earnings trajectories compared to cohorts who entered during stronger expansions.

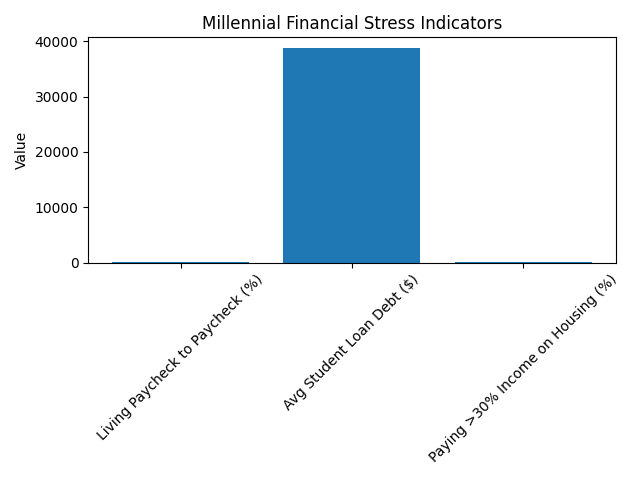

Student Debt Burden

Generation X carried student loans, but not at the scale millennials do. Outstanding federal student debt has surpassed $1.7 trillion nationally, with millennials holding a substantial share. The average borrower balance for millennials is significantly higher than what Gen X faced at comparable ages.

Debt servicing reduces disposable income, delays home purchases, and constrains entrepreneurship — all key drivers of long-term wealth accumulation.

Wealth Gap Comparisons

Federal Reserve data shows that at comparable ages, Generation X held more median household wealth than millennials. Asset appreciation — particularly in real estate and equities — disproportionately benefited older cohorts who already owned homes and investments before major price surges.

Millennials, by contrast, were less likely to own appreciating assets during critical expansion cycles. This timing disadvantage matters: wealth builds exponentially when gains compound over decades.

Inflation and Purchasing Power

The inflation spike of the early 2020s hit millennials during peak family-formation years. Grocery prices, energy costs, and insurance premiums rose rapidly, compressing household budgets. Even as inflation moderates, price levels remain permanently elevated.

For a generation already managing high rent, childcare, and debt payments, cumulative cost pressures reinforce the feeling of economic precarity.

Not a Narrative — A Structural Shift

Millennials are not uniformly struggling. High-income earners in tech, finance, and professional sectors have benefited from strong labor markets and asset growth. But aggregate data suggests the median millennial faces tighter affordability constraints than Generation X did at the same stage of life.

The frustration many millennials express is rooted in structural shifts:

- Asset price inflation outpacing wage growth

- Higher debt loads at entry into adulthood

- Delayed wealth accumulation cycles

- Greater exposure to economic shocks early in careers

The American Dream has not disappeared — but its entry price has risen sharply.

For millennials, the question is not whether they will eventually catch up. It is whether the economic architecture that once enabled broad middle-class mobility still functions the same way it did for those who came before them.

—Michael Lyles, B1Daily

Leave a comment