—Michael Lyles, B1Daily

The American beef market is increasingly becoming a case study in what happens when capitalism concentrates too much power into too few hands.

For years, economists warned that excessive consolidation inside critical industries would eventually distort pricing mechanisms, weaken competition, and create corporate bottlenecks capable of influencing entire sectors of the economy. Now many analysts believe the U.S. beef industry has become one of the clearest examples of that phenomenon in action.

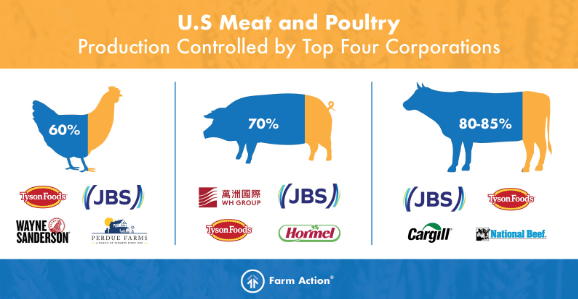

At the center of the controversy are four massive meatpacking corporations: Tyson Foods, Cargill, JBS USA, and National Beef Packing Company. Together, these firms control the overwhelming majority of America’s fed cattle processing capacity, creating what many economists classify as an oligopoly rather than a truly competitive free market.

That distinction matters enormously.

In a healthy competitive market, producers compete aggressively for supply while consumers benefit from price competition at the retail level. But in highly concentrated industries, dominant firms gain the ability to influence pricing structures, production capacity, and bargaining power across the entire supply chain.

The modern beef industry now sits directly in that debate.

Over the last several years, consumers have faced sharply rising beef prices at grocery stores and restaurants. At the same time, many cattle ranchers reported receiving disproportionately weak prices for their livestock despite elevated retail beef costs. Under normal market dynamics, strong consumer prices would typically increase upstream returns for producers. Instead, economists observed widening spreads between cattle prices and boxed beef prices, meaning processors captured increasingly large margins in the middle of the chain.

That economic imbalance triggered scrutiny from lawmakers, agricultural economists, and federal regulators.

Critics argue the structure of the beef industry itself creates pricing distortions. When only a handful of firms control slaughter capacity, ranchers often have limited bargaining leverage because there are few alternative buyers available within practical transportation distance. Economically, this creates what analysts call “monopsony power,” where a concentrated group of buyers can exert downward pressure on supplier prices.

In simpler terms, ranchers may be competing against each other far more aggressively than meatpackers compete against themselves.

At the consumer end of the market, concentration can also reduce competitive pressure to lower retail prices. If dominant firms maintain similar production behavior and pricing strategies, prices may remain elevated even when some input costs decline. This is where allegations of coordinated price fixing and supply manipulation have entered the public conversation.

Multiple lawsuits and federal investigations have accused major processors of restricting slaughter capacity and coordinating pricing behavior to maximize profits. The companies deny wrongdoing, arguing that supply disruptions, labor shortages, drought conditions, rising feed costs, and shrinking cattle inventories explain current price volatility.

And economically speaking, those pressures are real.

The U.S. cattle herd has fallen to some of its lowest levels in decades due to drought, land costs, and feed inflation. Lower cattle supply naturally raises prices. Meanwhile labor shortages and transportation expenses increased operational costs throughout the post-pandemic economy.

But critics counter that those factors alone do not fully explain the scale of processor profit margins observed during recent inflationary periods.

This is where the debate becomes larger than beef itself.

The beef industry increasingly reflects a broader structural issue inside the American economy: consolidation. Over the past forty years, mergers and acquisitions transformed multiple sectors into highly concentrated corporate ecosystems. Airlines, telecommunications, agriculture, banking, pharmaceuticals, media, and technology all experienced similar patterns where a small number of firms gained dominant market share.

Supporters of consolidation argue scale creates efficiency. Larger firms can reduce operational costs, stabilize supply chains, invest in technology, and achieve economies of scale that smaller competitors cannot match.

Critics argue excessive concentration eventually weakens competitive markets altogether.

The beef industry demonstrates both sides of that equation simultaneously. Large processors operate highly sophisticated logistical systems capable of processing enormous national demand efficiently. Yet that same concentration may also reduce market resilience and weaken price competition throughout the supply chain.

Economists often describe this dynamic as “too concentrated to fail competitively.” Once enough regional competitors disappear, dominant firms gain structural leverage simply because alternatives no longer exist.

That concern becomes especially serious in food industries because food inflation directly affects household purchasing power. Beef prices influence restaurant costs, grocery spending, and broader consumer inflation metrics. When concentration affects staple goods, the consequences spread beyond agriculture into the wider economy.

The result is growing political and economic pressure for antitrust enforcement.

Federal regulators are now examining whether America’s beef market crossed the line from efficient consolidation into anti-competitive dominance. If investigators conclude collusion or unlawful market coordination occurred, the industry could face major structural reforms, increased regulation, or expanded antitrust actions.

Regardless of how the legal cases unfold, one economic reality is becoming harder to dispute: America’s beef market no longer resembles the decentralized competitive system many consumers imagine.

It increasingly resembles a tightly controlled economic funnel where a handful of corporations sit at the narrowest point.

—Michael Lyles, B1Daily

Leave a comment