—Michael Lyles, B1Daily

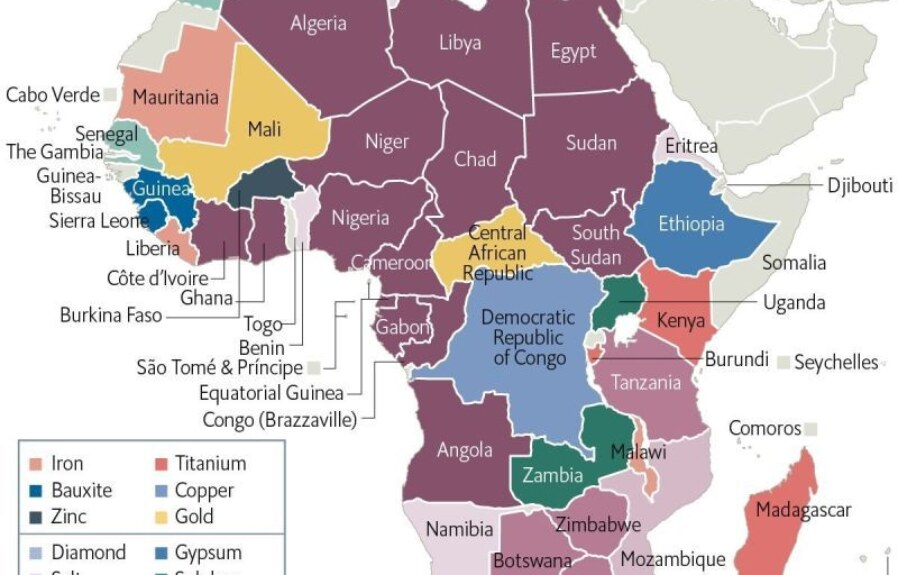

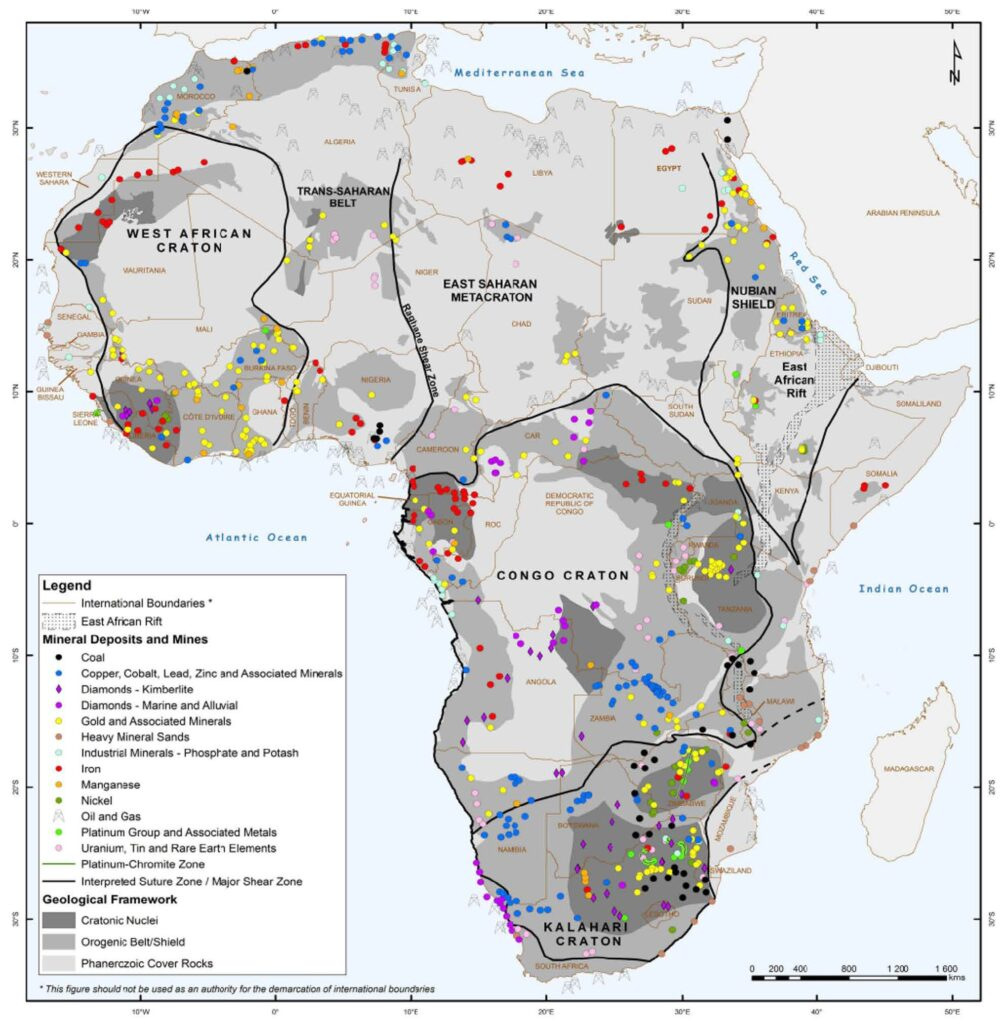

Africa sits on a geological jackpot, cobalt, lithium, rare earths, platinum group metals—the elemental backbone of the 21st-century economy. Yet the continent’s balance sheet tells a harsher story: export volumes rise, global demand explodes, and still the middle class thins while wealth concentrates at the top. The problem isn’t just what Africa sells. It’s how cheaply it sells it, and who captures the upside.

Start with pricing power, or the lack of it. Most African producers export unprocessed or minimally processed ore, where prices are set on international exchanges or through long-term offtake agreements dominated by large buyers. That keeps margins thin at the source. Refining, component manufacturing, and final assembly, the stages where value multiplies, happen elsewhere. In economic terms, Africa remains stuck at the low end of the value chain, where competition is fierce and pricing is weakest.

Layer on contract structures that lock in low prices. Many extraction deals were negotiated during periods of fiscal stress or political transition, when governments traded favorable terms for immediate investment. Stabilization clauses, tax holidays, and royalty ceilings can freeze a country’s take even as global prices surge. When cobalt spikes or lithium runs hot, the windfall largely accrues to firms operating downstream or to trading houses, not to the producing country.

Then there’s market structure. Buyers of critical minerals, battery manufacturers, major traders, and vertically integrated tech firms, operate with oligopsonistic leverage. Fewer buyers, many sellers. That imbalance pressures exporters to accept lower prices and stricter terms to secure guaranteed demand. Individual African states negotiating alone often face a take-it-or-leave-it menu.

Currency dynamics quietly worsen the deal. Commodities are priced in dollars, while local costs are in domestic currencies. During depreciations, export revenues translate into more local currency, which can mask weak pricing and reduce pressure to renegotiate terms. But over time, real income gains lag, especially once inflation catches up. The headline export numbers look strong; household purchasing power doesn’t.

Governance and revenue management complete the picture. Weak tax administration, opaque licensing, and illicit financial flows siphon off a portion of resource rents before they reach public budgets. Where revenues do arrive, they’re often volatile and politically contested. That volatility discourages long-term investments in education, infrastructure, and industrial policy, the very inputs that build a broad middle class.

The result is a classic rent concentration problem. A narrow slice of society, political elites, connected intermediaries, and segments tied to extractive firms, captures a disproportionate share of resource income. Without strong redistributive institutions or domestic value creation, those rents don’t diffuse through wages, small business growth, or productivity gains. You get a top-heavy income distribution: a visible upper tier and a stretched, fragile middle.

There’s also a strategic mispricing of risk. In the rush to attract capital, countries often underprice not just the minerals but the externalities, environmental degradation, infrastructure wear, and social costs. If those liabilities were fully priced into contracts, the effective “price” of extraction would be higher, and the fiscal return to the state could support broader development. Instead, future costs are discounted heavily, making current deals look deceptively attractive.

Global competition among African producers adds another downward pull. When neighboring countries offer sweeter terms to win the same investors, it becomes a race to the bottom on royalties, taxes, and local content requirements. Coordination is thin, so collective bargaining power never fully materializes.

None of this is inevitable. The policy toolkit is well understood, even if execution is hard:

Resource-backed pricing can be strengthened through auction-based licensing and periodic contract reviews that adjust royalties with price bands. Moving up the chain via domestic refining and processing captures more value per ton and builds industrial capability. Coordinated blocs, regional mineral alliances, can counter buyer power and stabilize terms across borders. Transparent revenue systems, sovereign wealth funds with clear rules, and investments in human capital convert volatile rents into steady gains for households.

There are early signs of a shift. Some countries are tightening export rules on unprocessed ores, others are renegotiating legacy contracts, and a few are courting downstream manufacturing in batteries and components. The goal isn’t to hoard resources, it’s to price them in line with their strategic importance and ensure the proceeds translate into jobs, wages, and durable growth.

Africa’s minerals are the scaffolding of the global energy transition. Selling them cheaply keeps the lights on elsewhere while dimming prospects at home. Repricing the continent’s resources, economically and politically, isn’t just about higher revenues. It’s about converting a geological advantage into a social one, where the middle doesn’t just exist, but expands and holds.

—Michael Lyles, B1Daily

Leave a comment